How the Money Moves: The Velocity Challenge in South Asia's Growth Story

As South Asia seeks to become one of the principal engines of global growth in the twenty-first century, velocity may emerge as one of the most important indicators of economic vitality. The countries that prosper most will not necessarily be those that create the most money, but those that use it most effectively.

Jul 04, 2026

Jul 04, 2026

South Asia - a region of over two billion people - is projected to remain one of the world's fastest-growing regions over the coming decade. India continues to rank among the fastest-growing major economies, Bangladesh has demonstrated remarkable resilience through export-led industrialisation, Nepal benefits from large remittance inflows, Bhutan is pursuing a distinctive path of sustainable development, Sri Lanka is emerging from a severe economic crisis. Pakistan is grappling with recurring macroeconomic instability, while Afghanistan faces the daunting challenge of economic reconstruction. Despite their diverse economic trajectories, these countries share a common but often overlooked monetary phenomenon: the declining velocity of money.

Public debate on economic policy generally focuses on inflation, interest rates, fiscal deficits and money supply. Yet an equally important variable receives far less attention. The effectiveness of money in generating economic activity depends not only on how much money exists but also on how rapidly it circulates through the economy.

This relationship is captured by the famous accounting identity MV = PY where M is money supply, V is the income velocity of money, P is the price and Y is nominal output.

The equation of exchange links the money supply, the income velocity of money, the price level and nominal output.. Economic activity depends not merely on the stock of money but also on how efficiently that money moves through households, businesses and financial institutions.

Velocity measures the number of times a unit of money changes hands during a given period. A higher velocity implies active spending, investment and production. A lower velocity indicates that money is being held in deposits, savings instruments or precautionary balances rather than being used in economic transactions.

Understanding Broad Money

To understand velocity, it is necessary to understand what economists mean by money. Not all money exists as currency in circulation. Modern economies operate through a combination of cash, bank deposits and other financial instruments. A distinction is therefore made between narrow money and broad money.

Narrow money, commonly known as M1, consists of currency held by the public and demand deposits that can be used immediately for transactions.

Broad money, generally referred to as M3, includes M1 plus time deposits and other savings balances held within the banking system. It therefore captures both transaction money and a large portion of household and business savings. For policymakers, M3 is often the most useful measure because it reflects the overall liquidity available within an economy.

The distinction is important because a country may experience rapid growth in broad money even when spending and investment remain subdued. If households place increasing amounts of their income in bank deposits, pension funds, insurance products or other financial assets, M3 expands faster than economic activity, causing velocity to decline. This pattern has become increasingly visible across South Asia.

The Financial Deepening Story

Over the past three decades, South Asian economies have experienced significant financial deepening. Banking networks have expanded dramatically. Financial inclusion programmes have brought millions into the formal financial system. Digital payment platforms have transformed transactions. Remittance inflows have increased household savings. As a result, broad money has generally grown faster than GDP. The ratio of broad money to GDP provides a useful measure of financial depth. The inverse ratio—GDP divided by broad money—serves as a measure of velocity.

We have used 2024 (or FY2023–24/FY2024–25 where applicable) as the common reference period for comparable monetary

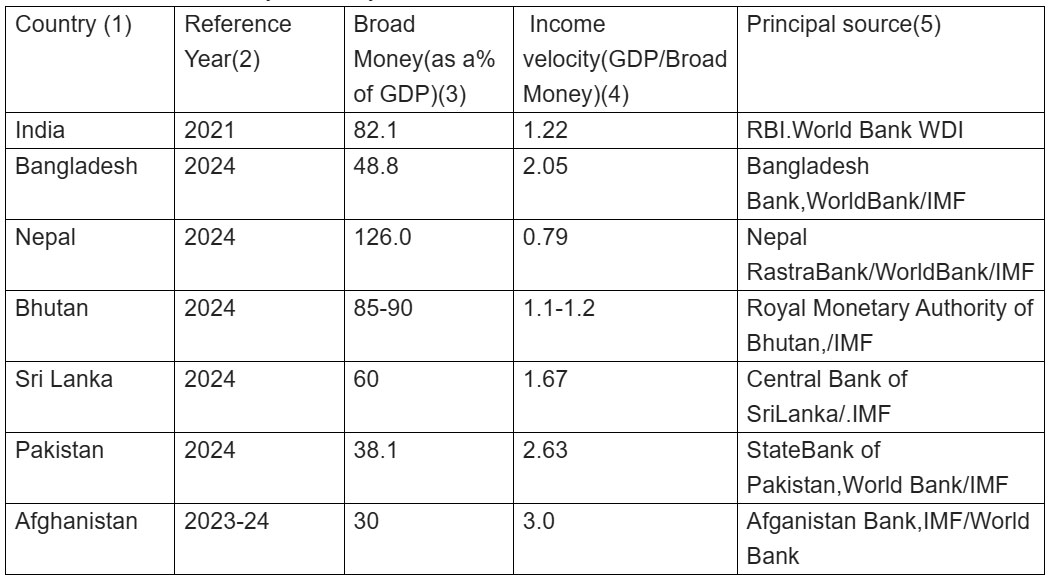

Values of Income Velocity of Money

Note:1 Figures for Bhutan and Sri Lanka are approximate

Note:2 Income velocity of broad money.(col.4) is calculated as nominal GDP divided by broad money (M3)

For India, each rupee of the total money stock supports on average 1.22 worth of nominal GDP over the course of a year. Similarly the figures for other countries show how much each unit of their money stock supports their nominal GDP.

India: The Rise of Financialisation

India provides perhaps the clearest illustration of this phenomenon.

Since the economic reforms of 1991, India's banking system has expanded enormously. Financial inclusion initiatives such as Jan Dhan Yojana, Aadhaar-linked services and digital banking have transformed access to finance.

Broad money has risen substantially relative to GDP. During the early 1990s, the GDP-to-M3 ratio was approximately 1.5. Today it is closer to 1.2.

This decline reflects the increasing financialisation of savings. Households now hold larger portions of their wealth in deposits, mutual funds, insurance products and pension schemes.

The Covid-19 pandemic accelerated the trend. Uncertainty encouraged precautionary savings while monetary accommodation increased liquidity. As a result, money supply expanded faster than economic activity and velocity fell further.

Bangladesh: Manufacturing and Faster Circulation

Bangladesh offers a contrasting model. Its export-oriented garment sector has generated extensive production networks requiring continuous movement of working capital. Funds circulate rapidly among factories, suppliers, workers and exporters. Consequently, Bangladesh exhibits a relatively higher velocity despite strong economic growth.

The country demonstrates that velocity is influenced not only by financial depth but also by the structure of production. Manufacturing-intensive economies often sustain faster circulation because production chains generate repeated transactions.

As Bangladesh progresses toward upper-middle-income status, policymakers will need to balance financial deepening with continued dynamism in the real economy.

Nepal: Remittances and Idle Balances

Nepal's experience highlights another important dimension. Remittances contribute more than a quarter of national income and represent one of the world's highest remittance-to-GDP ratios. These inflows support household consumption and generate substantial bank deposits. Consequently, Nepal's broad-money ratio exceeds 120 per cent of GDP. However, productive investment opportunities have not expanded at the same pace. Large volumes of financial resources therefore remain within the banking system, contributing to low velocity. The challenge facing Nepal is less about generating savings and more about mobilising them productively.

Bhutan: Small but Financially Deep

Bhutan presents a unique case. Hydropower exports, strong state institutions and prudent financial regulation have created a relatively deep financial system for a small economy. As in the case of Nepal and India, Bhutan displays comparatively low velocity because substantial resources remain within formal financial institutions. As Bhutan seeks economic diversification, converting accumulated savings into productive private-sector investment will become increasingly important.

Sri Lanka: Crisis and Confidence

Sri Lanka's recent economic crisis demonstrates how velocity is affected by expectations and confidence. The balance-of-payments crisis of 2022 generated inflation, shortages and uncertainty. Households increased precautionary savings while firms postponed investment decisions. Under such conditions, even substantial liquidity may fail to stimulate economic activity. The Sri Lankan experience underscores an important lesson: monetary policy alone cannot restore growth. Confidence, institutional credibility and macroeconomic stability are equally important determinants of velocity.

Pakistan: High Velocity, Low Financial Depth

Pakistan's financial structure differs significantly from India's. Broad money constitutes a smaller share of GDP, indicating lower financial depth and weaker intermediation. As a result, measured velocity appears relatively high. However, high velocity is not necessarily a sign of economic strength. It may also reflect a limited capacity to mobilise long-term savings and channel them into productive investment.

Persistent inflation, exchange-rate volatility and recurrent balance-of-payments pressures have complicated monetary management and constrained financial development.

Afghanistan: Monetary Constraints in a Fragile Economy

Afghanistan occupies a distinct position within South Asia. Years of conflict, political instability and institutional fragility have severely limited banking penetration and financial development. A substantial share of economic activity remains outside formal financial channels. Consequently, traditional monetary indicators provide only a partial picture of economic activity.

Afghanistan highlights the fundamental proposition that : velocity becomes meaningful only when supported by functioning financial institutions and credible monetary frameworks.

Digital Payments: Faster Transactions, Not Necessarily Higher Velocity

One of the most important questions facing South Asia is whether digitalisation can reverse declining velocity. India's Unified Payments Interface (UPI) has transformed the payments landscape. Bangladesh, Pakistan, Nepal and Sri Lanka have also expanded digital payment systems. However, digitalisation should not be confused with higher velocity. A payment completed instantly rather than over several days improves efficiency, but it does not necessarily increase spending. Velocity depends primarily on income growth, business confidence, investment opportunities and consumer behaviour. Digital payments make transactions easier. They do not automatically make people spend more. Nevertheless, digitalisation contributes to economic efficiency, formalisation and financial inclusion, thereby strengthening the foundations for long-term growth.

Lessons from Advanced Economies

South Asia is not unique. The United States, Japan and the Euro Area have also experienced declining velocity over several decades. As financial systems mature, households hold larger financial balances relative to annual spending. Pension funds, insurance products and long-term savings instruments grow faster than transaction demand.

South Asia appears to be following a similar trajectory, although at a much lower level of per-capita income. This suggests that declining velocity is not necessarily a sign of economic weakness. In many cases, it reflects the natural consequence of financial development.

The Real Policy Challenge

The conventional policy debate often assumes that more money generates more growth. The South Asian experience suggests otherwise. Many countries in the region have successfully expanded financial inclusion and increased access to formal banking. Yet monetary expansion alone has not guaranteed stronger investment or employment. The challenge is therefore shifting from creating money to mobilising money. Governments must ensure that financial savings are channelled into productive sectors such as infrastructure, manufacturing, renewable energy, technology, education and healthcare. Central banks must monitor not only money supply but also changes in velocity and the demand for money.

A rapid increase in money supply may have little inflationary effect if velocity is falling. Conversely, inflationary pressures may emerge even without extraordinary monetary expansion if velocity begins rising sharply. Understanding this interaction will become increasingly important for policymakers across South Asia.

Channelling Money Into Investment

South Asia possesses many advantages: a young population, expanding urbanisation, growing digital connectivity and significant potential for industrialisation. Yet long-term prosperity will depend not merely on the quantity of money available but on how effectively that money is deployed.

India, Bangladesh, Nepal, Bhutan, Sri Lanka, Pakistan and Afghanistan differ enormously in economic size, institutional capacity and development levels. Nevertheless, they face a common challenge: ensuring that growing financial resources are transformed into productive investment rather than remaining trapped in financial balances.

The real monetary question confronting South Asia is therefore not whether enough money exists. It is whether that money moves. As the region seeks to become one of the principal engines of global growth in the twenty-first century, velocity may emerge as one of the most important indicators of economic vitality. The countries that prosper most will not necessarily be those that create the most money, but those that use it most effectively.

(The writer is a retired Special Secretary, Government of India, and a commentator on financial, geoeconomic and regional issues. The views expressed are personal. He can be reached at ppmitra56@gmail.com.)

Post a Comment