Road to economic revival in South Asia looks difficult but not impossible

Of the 176 million people expected to be pushed into poverty at the $3.20 per day poverty line, two-thirds are in South Asia. The addition is due to the raising of the poverty estimating line, which has been termed as the new poor, writes Partha Pratim Mitra for South Asia Monitor

Nov 09, 2020

Nov 09, 2020

A combination of domestic outbreaks of the COVID-19 pandemic and the resultant lockdowns hit growth hard in developing Asia and South Asia, the hardest. Growth rates in the first half of 2020 were substantially below 2019 and in most economies it actually contracted.

Private consumption - normally a stable source of demand and one of the prime drivers of regional growth for the past decade - contracted in the first half in many countries as a result of sudden and unprecedented job losses and a lack of purchasing power.

Investment also took a hit affecting imports and net exports, affecting growth, particularly in economies that rely heavily on export.

Huge impact of COVID-19 in Asia and Pacific region

The Asia and Pacific region’s recent achievements in reducing extreme poverty are greatly affected by the COVID-19 pandemic and the ensuing global recession caused by lockdown measures to contain the virus. The World Bank estimates that between 71 million and 100 million people around the world may be pushed into extreme poverty in 2020.

In developing Asia, the percentage of people living in extreme poverty -those surviving on less than $1.90 per day (equivalent purchases that the amount can make in all countries at 2011 prices) increased. As a percentage of the overall population, extreme poverty fell in every sub-region in developing Asia from 2002 to 2015: Central and West Asia (from 29.3 percent in 2002 to 5.8 percent in 2015), East Asia (from 31.6 percent to 0.7 percent), Southeast Asia (from 24.8 percent to 5.4 percent) and South Asia (from 39.7 percent to 13.2 percent).

When we look at each of the countries of the South Asian region, poverty is expected to increase in 2020. In Afghanistan, the poverty-headcount ratio would reach 54.5 percent of the population; Bangladesh ($1.9 per day )-14.5 percent; Bhutan ($1.9 per day) -1.5 per cent; India ($1.9 per day) 21.2 percent; Maldives ($5.5 per day ) 3.4 percent; Nepal ($1.9 per day)-15.0 per cent; Pakistan ($1.9 per day)- 4.0 per cent, and Sri Lanka ($1.9 per day) 0.9 percent.

New poor

At higher international poverty estimating levels the regional distribution of the poor increases markedly, according to the World Bank. Of the 176 million people expected to be pushed into poverty at the $3.20 per day poverty line, two-thirds are in South Asia. The addition is due to the raising of the poverty estimating line, which has been termed as the new poor.

The new poor are those who were expected to be non-poor in 2020 before the COVID-19 outbreak but are now expected to be poor in 2020. Profiles of the new poor in 2020 are likely to be somewhat different from the profiles of the chronic poor in both 2019 and 2020 and significantly different from those of the non-poor in 2020. This is likely to be so since most of the new poor are essentially those who would have been just above the poverty line in every country in 2019.

The new poor are projected to be more likely to live in urban areas live in dwellings with better access to infrastructure, own slightly more basic necessary assets than those who are chronic poor in both 2019 and in 2020. The new poor who are 15 years and older of age are more likely to be paid employees and work more in non-agriculture (manufacturing, service, commerce sectors) then the chronic poor. The new poor tend to be more educated than the chronic poor, and significantly less educated than the non-poor (of age 15+ years). It has been observed that the share of employed among the new poor would be lower than the chronic poor and unemployment rate higher than the non-poor. South Asia region has this new poor in large numbers.

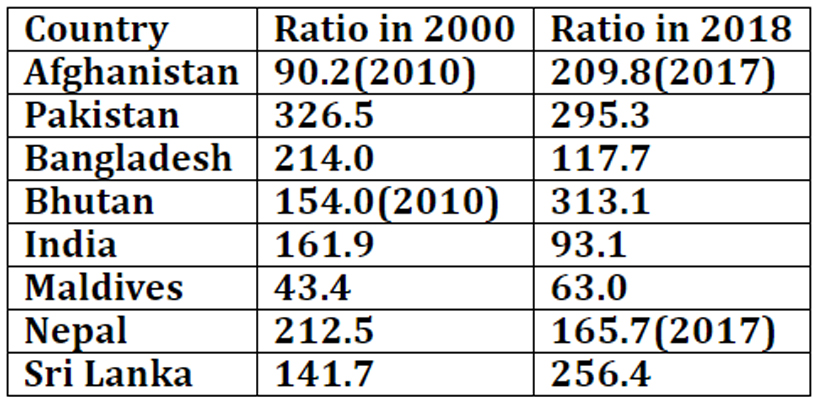

Vulnerabilities of countries would remain high, with depleted fiscal resources, high indebtedness, and larger financial requirements for the recovery process. The extent to which economies become vulnerable would depend on the performance of economies over a period of time in different sectors. On the external of debt, some of the South Asian economies have a difficult task ahead of servicing it. Between 2010 and 2018, for most economies either the ratio of external debt to exports and net income from abroad (primary income) has either gone up or has remained significant. (See table 1)

Table I: External debt as percentage of export of goods, services & primary income

Source: Key indicators for Asia and Pacific, ADB

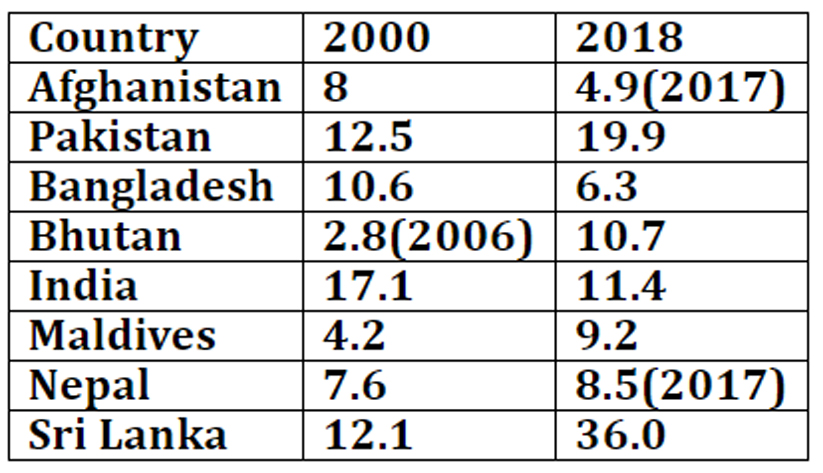

The debt service which goes into repaying the external debt of countries in the region are measured by the proportion of export earnings from goods, services, and income from abroad as apportion of the county’s total debt. The picture which emerges is the rise in the average debt service burden from 9.5 percent in 2000 to 13.4 percent in 2018 for South Asia. With only two countries having a debt service burden above the regional average in 2018 as compared to four countries in 2000, the debt service burden is yet not a major problem in the region. (see Table 2).

Table 2: Debt service payment (percentage of exports of goods, services, and net income from abroad)

*Not mentioned

Source: Key indicators for Asia and Pacific, ADB

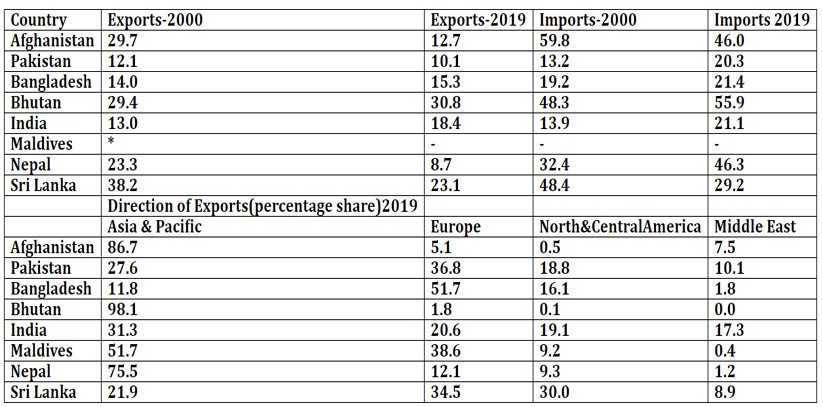

The exports and imports as a proportion of the Gross Domestic product (GDP) of individual countries shows that the share of exports in GDP has grown at a slower pace than the share in imports. Sri Lanka, India and Bangladesh have, however, managed to restrict increases in the share of imports in keeping with the change in the share of exports in GDP. Nepal and Bhutan have continued to maintain a higher share in imports to GDP despite the share of exports increasing marginally for Bhutan while declining sharply for Nepal. (See table 3).

The share of the foreign trade sector in the GDP (exports and imports combined) for most countries in the region has increased except Afghanistan, Nepal and Sri Lanka. These three countries have also a high external debt as a proportion of export earnings and primary income along with Pakistan.

Table3: Exports and imports as a percentage of GDP in South Asia

*Not mentioned

Source: Key indicators for Asia and Pacific, ADB

Data on the direction of exports shows that India, Pakistan and Sri Lanka has a diversified export market as they are not excessively dependent on any particular region. Such diversification is likely to be helpful as they do not have to depend on the economic conditions of any particular region. However, during a pandemic when all global markets are affected such diversification may not matter much but business links and market specialization becomes important and diversification gives an added edge to contain business risks across regions.

However, given the high ratios of external debt to export earnings of most countries in South Asia, diversification of the export markets would be important to garner higher export earnings.

Road to recovery

The key message which emerges is that any development strategy with the involvement of external debt would necessarily have to depend on export earnings and primary income from abroad to service the external debt. Sri Lanka, Nepal, and Bhutan have a significant share of services in GDP, so do the other countries of the region. Both Sri Lanka and Bhutan have a higher share of industries in their GDP than other countries of the region. India and Bangladesh also have a high share of industries in GDP in comparison to other countries in the region.

These countries have a good opportunity to join the global value-chain and participate in the integrated global manufacturing structure which is fast emerging with the relocation of industries taking place in some parts of the world.

South Asia could participate in the global economic revival but the road to recovery seems difficult but not impossible provided appropriate policy measures on the fiscal and monetary front to revive consumption and investment demand to restart the growth and the development cycle in the region is taken.

(The writer is a retired Indian Economic Service officer who worked in the labour ministry. The views expressed are personal. He can be contacted at ppmitra56@gmail.com)

References:

Key Indicators for Asia and the Pacific, Asian Development Bank, September 2020https://www.adb.org/sites/default/files/publication/632971/ki2020.pdf

South Asia, Annual Meetings, October 2020,p1-20 The World Bank,http://pubdocs.worldbank.org/en/830011554478869647/mpo-sar.pdf www.worldbank.org

Mayler, Daniel etal, Updated estimates of the impact of COVID-19 on global povertyhttps://blogs.worldbank.org/opendata/updated-estimates-impact-covid-19-global-poverty,june 8,2020

Minh Cong Nguyen, Nobuo Yoshida, Haoyu Wu and Ambar NarayanProfiles of the new poor due to the COVID-19 pandemicAugust 6, 2020http://pubdocs.worldbank.org/en/767501596721696943/Profiles-of-the-new-poor-due-to-the-COVID-19-pandemic.pdf

Post a Comment