South Asia: Fiscal policy as an option for economic revival

The data on the growth rates in Gross Domestic Product between 2015 to 2020 show that South Asia would show the maximum decline in 2020 after growing the fastest between 2015-2019 at an annual average rate of 6.1 percent as compared to 4.8 percent for Southeast Asia and 6.0 percent for East Asia, writes Partha Pratim Mitra for South Asia Monitor

Jul 07, 2020

Jul 07, 2020

During COVID-19, globally the mix of fiscal policy measures by the government and central bank monetary policy responses have been the focus to ensure that there is sufficient liquidity available in people's hands through cash transfers from the exchequer and into the real economy, particularly for small and medium-sized enterprises, to bridge the temporary cash flow constraints and minimize unemployment through employment generation schemes. As the COVID-19 crisis became deeper and more prolonged, the clamor for government help from larger companies in hard-hit sectors intensified; support has often been forthcoming in response. A problem which has often been articulated in many policy circles is that there has not been a globally coordinated response to the crisis, and the piecemeal policy responses have increased uncertainties and resultant volatility in financial markets.

A direct impact of the pandemic-induced economic slowdown has been on informal employment, which tends to be more in developing economies. It is estimated that around 80 percent of the global workforce was affected by full or partial workplace lockdowns. The International Labour Organization (ILO) estimates that the pandemic caused a decline of 4.5 percent in working hours (equivalent to 130 million full-time jobs) globally in the first quarter of 2020, compared with the pre-pandemic level. The decline is expected to widen to 10.5 percent in the second quarter, which is equivalent to 305 million full-time workers. It is estimated that Asia and the Pacific suffered the most among world regions in the first quarter (a 6.5 percent decline or 115 million jobs) and a 10 percent decline in the second quarter. Informal sector workers in the region (7 in 10 workers) have become more vulnerable given their limited access to social protection and low wages.

South Asia shows the highest share (89 percent) in informal employment, followed by Southeast Asia (76 percent) and Central Asia (70 percent). Bangladesh, India, and Nepal, where at least 9 in 10 workers are informal, would be at higher risk of impoverishment because of the crisis. The hardest hit among the economic sectors during COVID-19 will be accommodation and food services, manufacturing, wholesale and retail trade, and real estate and business activities, according to the ILO’s assessment using the latest economic and financial data. Wholesale and retail trade and accommodation and food services, accounting for 16 percent (115 million workers) of total employment in the region, has been severely impacted by almost full closure, aggravated by a fall in demand.

More than half of the workers in these sectors are also female in all subregions of Asia, except for South Asia. Manufacturing (with 13 percent of total employment in the region), has also suffered severe domestic and global value chain disruptions. Such disruptions include automobiles and textiles, clothing, and leather and footwear, among others.

We shall look at certain data-points on South Asia on the economic situation before the pandemic and in the wake of it. The data on the growth rates in Gross Domestic Product between 2015 to 2020 show that South Asia would show the maximum decline in 2020 after growing the fastest between 2015-2019 at an annual average rate of 6.1 percent as compared to 4.8 percent for Southeast Asia and 6.0 percent for East Asia. (see Table 1)

Table :1 Growth rates of Gross Domestic Product for Asian sub-regions (in percent)

Source: Asian Development Bank Data Library, June 2020

(The table shows annual growth rates of GDP valued at constant market price, factor cost, or basic price. GDP at market price is the aggregation of value added by all resident producers at producers’ prices including taxes less subsidies on imports plus all nondeductible value-added or similar taxes. Constant factor cost measures differ from market price measures in that they exclude taxes on production and include subsidies. Basic price valuation is the factor cost plus some taxes on production, such as those on property and payroll taxes, and less some subsidies, such as those on labor-related subsidies but not product-related subsidies. Most countries use constant market price valuation.)

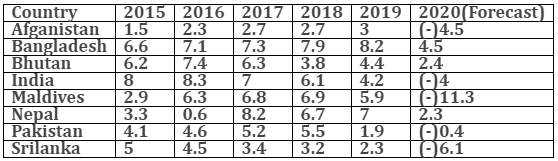

The average annual growth rates of GDP between 2015-2019 of South Asian countries tell us that each country was on a different growth trajectory and hence the intensity of the pandemic on countries would be different depending on their individual growth rates and the forecast. Only India (6.7 percent) and Bangladesh (7.4 percent) have registered a higher annual average growth rates above the overall average growth rate for South Asia (6.1 percent) during the period 2015-2019 and the forecast shows that the Maldives would be affected the most followed by Srilanka, India and Afghanistan. (see table 2)

Table 2: Growth of Gross Domestic Product for South Asian Countries(in percent)

Source: Asian Development Bank Data Library, June 2020

(The table shows annual growth rates of GDP valued at constant market price, factor cost, or basic price. GDP at market price is the aggregation of value added by all resident producers at producers’ prices including taxes less subsidies on imports plus all nondeductible value-added or similar taxes. Constant factor cost measures differ from market price measures in that they exclude taxes on production and include subsidies. Basic price valuation is the factor cost plus some taxes on production, such as those on property and payroll taxes, and less some subsidies, such as those on labor-related subsidies but not product-related subsidies. Most countries use a constant market price valuation.)

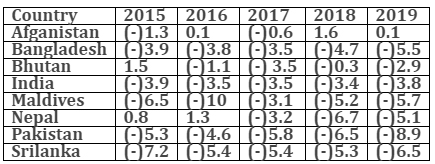

We would next, see the fiscal space available to each country of the South Asian region to meet the crisis. The data shows that the Maldives and Srilanka which are expected to be affected more by the crisis, have high fiscal balances (fiscal deficit as a percentage of GDP)) but Nepal, Bangladesh, and Pakistan has growing fiscal balances between 2015 and 2019, thereby reducing its fiscal maneuverability to manage the crisis. (see table 3)

Table 3: Fiscal balances (Fiscal deficit as a percentage of Gross Domestic Product)of South Asian Countries

Source: Asian Development Bank Data Library, June 2020

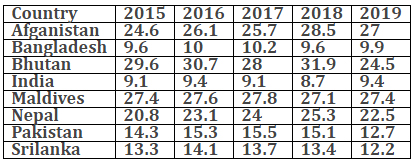

We would next see the revenue trends of the central government as a percentage of Gross Domestic Product to assess the fiscal strength of countries to face the crisis. Most countries have experienced either stagnant or decline in revenue earnings, making it all the more difficult to face the COVID-19 challenge. (see table 4 )

Table 4: Central government revenue as a percentage of Gross Domestic Product

Source: Asian Development Bank Data Library, June 2020

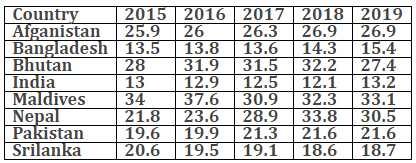

We would also see the trends in central government expenditure in these countries to assess the fiscal rearguard action to steer them out of the crisis. The trends seem to be mixed with countries facing the crisis more then the rest (Maldives, Srilanka, India, and Afganisthan) have either stagnant or declining central government expenditure (see table 5)

Table 5:Central government expenditure as a percentage of Gross Domestic Product

Source: Asian Development Bank Data Library, June 2020

The options open to countries, therefore, would need to take into consideration the extent of the looming crisis facing each of them. The fiscal option available to them would give them the leverage to go in for further direct intervention packages given the dimensions of the crisis. The other options which are in the realm of monetary policy would give them the additional option of infusing liquidity into the economy to revive demand and facilitate access of loans from financial institutions to kick-start businesses. The guarantees for credit advanced by financial institutions in the case of defaults by businesses would, however, depend on the fiscal health of governments as these guarantees are essentially contingent liabilities on the government exchequers. Fiscal measures, therefore play a more important role than other measures to take the economies out of the COVID-19 pandemic and stabilize them for post- pandemic revival.

(The writer is a retired Indian Economic Service officer who worked in the labour ministry. The views expressed are personal. He can be contacted at ppmitra56@gmail.com)

Reference:

ASIA BOND MONITOR JUNE 2020https://www.adb.org/sites/default/files/publication/612686/asia-bond-monitor-june-2020.pdf

ADB BRIEFS NO. 139 JUNE 2020

https://www.adb.org/sites/default/files/publication/611671/adb-brief-139-food-security-asia-pacific-covid-19.pdf

ibid

Post a Comment