The Greenium Paradox: Can South Asia Align Climate Finance with Investor Demands?

In June 2025, Sri Lanka’s DFCC Bank broke new ground as the first foreign corporation to list a green bond on India’s NSE International Exchange in GIFT City. The $8 million bond financed solar energy projects aligned with Sri Lanka’s 2030 renewables target. By securing a dual listing in Luxembourg and aligning with ICMA’s Green Bond Principles, DFCC broadened its international investor appeal and demonstrated how green finance can support debt stressed economies.

Sep 18, 2025

Sep 18, 2025

Over the past decade, financial markets have witnessed a transformation: the rapid rise of green bonds. These instruments, designed to finance projects with environmental and ecological benefits, are reshaping how private capital and governments think about sustainability and capital markets. From funding renewable energy to improving climate resilience, green bonds have moved from being niche instruments to mainstream tools to facilitate the global transition to a low-carbon economy.

Green bonds are debt securities issued for raising capital specifically for environmentally friendly projects, such as renewable energy, energy efficiency, sustainable transport, or biodiversity conservation. Unlike traditional conventional bonds, where funds can be used for any purpose, green bonds require proceeds to be earmarked for green projects. This demarcation increases transparency and attracts environmentally conscious investors.

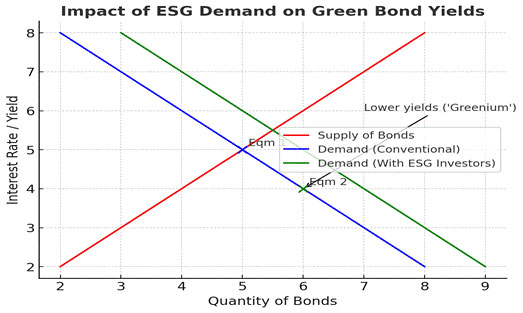

One crucial concept in this market is the greenium - a term used for describing the lower yield investors are often willing to accept on green bonds compared to regular bonds. This happens because demand for sustainable investments is so strong that issuers can borrow at slightly cheaper rates.

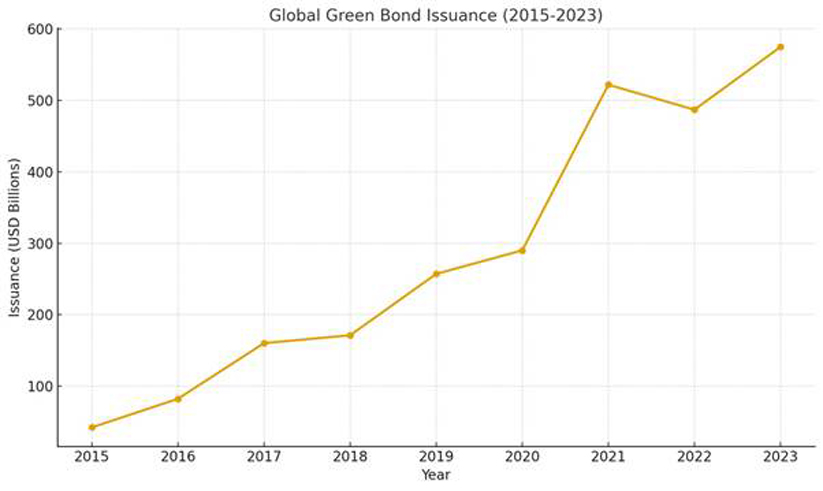

The growth of the green bond market has been exponential. From a mere $3 billion issuance in 2012, it had surpassed $1 trillion in cumulative issuance by 2020 and is expected to reach $5 trillion by the end of 2025.

The rapid increase, particularly after the 2015 Paris Agreement demonstrates how climate policy and investor demand have fueled growth.

The sustainable debt market in Asia has been growing fast. In 2024, Asian corporations issued $145 billion in sustainable bonds, with green labelled instruments making up two-thirds of that volume. India alone saw its cumulative GSS + ( green, social, sustainability, sustainability - linked ) debt hit $55.9 billion by the end of 2024 - a 186% jump from 2021. This boom suggests South Asia could realize strong greenium gains - if market conditions align well.

Recent research reinforces that promise. A 2023 IMF working paper estimated the average sovereign greenium globally at ~ 4 basis points ( bps ) in advanced economies, and ~11 bps in Emerging Market Economies. The same study found greenium increasing over time. Certified green bond deals also tend to deliver higher premiums; green bonds in Asia with credible verification show averages closer to ~ 12 bps under favorable conditions. These findings suggest that South Asia, as part of EMEs with strong ESG demand and credible issuers, should be among the beneficiaries.

India Cancelled Auctions

Unfortunately, South Asia’s experience tells a more complicated story - especially in India. India's first sovereign green bonds in January 2023 did capture a greenium of approximately 5-6 bps, with yields 5-6 bps lower than similar government securities for 5 and 10 year tenors. But later auctions faltered. In May 2024 and June 2025, India cancelled planned green bonds auctions after investors demanded yields higher than the government was willing to accept. The greenium appears to have shrunk to near zero, or even turned negative in these auctions.

Macro-risks are part of the reason: local currency depreciation, inflation, commodity shocks, and global interest rate volatility have made investors less willing to accept small yield concessions for green backing. The oversight ? This green label alone does not insulate sovereign issuers from broader financial risks.

Not A Silver Bullet

However, not all stories are bleak. Sub-sovereign and corporate issuers are finding ways to thrive. In June 2025, Sri Lanka’s DFCC Bank broke new ground as the first foreign corporation to list a green bond on India’s NSE International Exchange in GIFT City. The $8 million bond financed solar energy projects aligned with Sri Lanka’s 2030 renewables target. By securing a dual listing in Luxembourg and aligning with ICMA’s Green Bond Principles, DFCC broadened its international investor appeal and demonstrated how green finance can support debt stressed economies.

Ultimately, green bonds are not a silver bullet. Their pricing benefits may prove cyclical and the greenium itself may remain quite elusive. Yet as DFCC Cases illustrates, when projects are credible and transparent, investors are ready to channel heavy capital.

References :

IMF Working Paper No. 2023/080: “How Large is the Sovereign Greenium?” (April 2023) https://www.imf.org/en/Publications/WP/Issues/2023/04/07/How-Large-is-the-Sovereign-Greenium-530332

Reuters: “India’s first green bond issue pulls local bidders, foreigners aloof – 5-6 basis points below sovereign yields” https://www.reuters.com/world/india/india-sells-first-green-bonds-5-6-basis-points-below-sovereign-yields-2023-01-25

Reuters: “India’s first green bond sale to command ‘greenium’ on strong demand” (Jan 24, 2023) https://www.reuters.com/world/india/indias-first-green-bond-sale-command-greenium-strong-demand-sources-2023-01-24

Climate Bonds Initiative: “India’s debut in the sovereign green bond market: first deal landed a greenium!” https://www.climatebonds.net/2023/03/india%E2%80%99s-debut-sovereign-green-bond-market-first-deal-landed-greenium

Reuters: “India cenbank devolves 70% of new green bonds …” (Nov 2024)

https://www.reuters.com/world/india/india-cenbank-devolves-70-new-green-bonds-cutoff-below-10-year-note-2024-11-29

Reuters: “India may not issue green bonds this fiscal due to lack of ‘greenium’.” (Sep 2023)

https://www.reuters.com/article/world/india-may-not-issue-green-bonds-this-fiscal-due-to-lack-of-greenium-source-idUSKBN30B0V0

ESG Today: “India’s Inaugural Green Bond Earns ‘Greenium’ on Solid Demand.” (Jan 2023)

https://www.esgtoday.com/indias-inaugural-green-bond-draws-greenium-on-solid-demand

Energypolicy.columbia.edu: “India Integrates Green Bonds Into Its Decarbonization Strategy.” (Mar 2023)

https://www.energypolicy.columbia.edu/india-integrates-green-bonds-into-its-decarbonization-strategy

Reuters: “India’s first green bonds to fund new climate finance projects.”https://www.reuters.com/business/environment/india-govt-use-proceeds-green-bonds-fund-renewable-energy-clean-transportation-2022-11-09

Reuters: “Vadodara Municipal Corporation issues Asia’s first certified green municipal bond’s https://www.reuters.com/world/india/indias-gujarat-state-civic-body-issues-asias-first-certified-green-municipal-2024-03-01

IMF Climate Finance Monitor Q1 2023 – EMDE issuance trends https://www.imf.org/-/media/Files/Publications/WP/2023/English/wpiea2023080-print-pdf.ashx

Reuters: “India’s first green bond to attract mix of local, foreign buyers.” (Nov 2022)https://www.reuters.com/markets/rates-bonds/indias-first-green-bond-attract-mix-local-foreign-buyers-bankers-2022-11-11

Reuters: “India’s first green bond issue … 5-6 bps below sovereign yields.” https://www.reuters.com/world/india/india-sells-first-green-bonds-5-6-basis-points-below-sovereign-yields-2023-01-25

ResearchGate summary: “green vs non-green yield spreads 4-8 bps on average” https://www.researchgate.net/publication/4423375_Green_vs_Non-Green_Yield_Spreads

The SOAS Working Paper: “The Price of Trust: Greenium and Greenwashing in Asia’s Green Bond Markets.”https://www.soas.ac.uk/research/research-publications/

(The writer is a student at Delhi Public School, Noida, India. Views expressed are personal. He can be reached at mrigankswork@gmail.com)

Post a Comment