South Asia: An assessment for a post-COVID economic recovery

The dilemma of growing COVID-19 cases and reviving economic activity is crucial at this juncture which the leadership in the South Asia region will have to resolve and, herein, lies the challenge for it, writes Partha Pratim Mitra for South Asia Monitor

Sep 25, 2020

Sep 25, 2020

An assessment for a post-COVID-19 economic recovery of any region needs to take into consideration the economic fundamentals that prevailed in the region before the pandemic to bring out its ability to recover.

To do so, we have presented some of the factors that constitute the economic fundamentals in South Asia. The factors that have been taken into consideration are: Household consumption expenditure percent of GDP, growth of household consumption expenditure, growth of GDP, government revenue as a percentage of GDP, and overall budgetary surplus/deficit as a percent GDP.

We will analyse these factors to show them criticality in the recovery process and to understand the policy interventions that would be required to make the recovery process more robust.

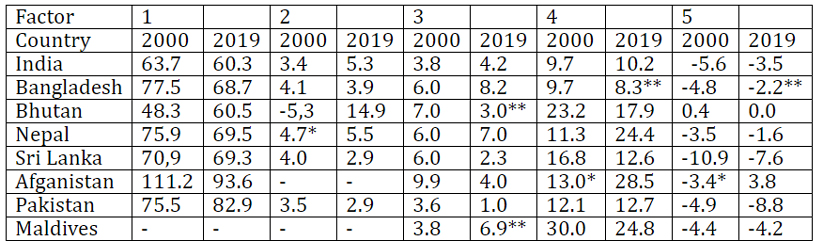

Table 1: Trends in economic factors that would shape a post-COVID economic recovery

Source: Asian Development Bank, Key Indicators Database,2020, https://kidb.adb.org

Note: Household consumption expenditure percent of GDP, growth of household consumption expenditure, growth of GDP, government revenue as a percentage of GDP, and overall budgetary surplus/deficit as a percent GDP.

The structure and the growth of demand in the region is important, as many critics consider that the demand constraint is at the core of the economic problem in the region and it would be absolutely necessary to resolve this problem if growth is to happen on a self-sustained basis.

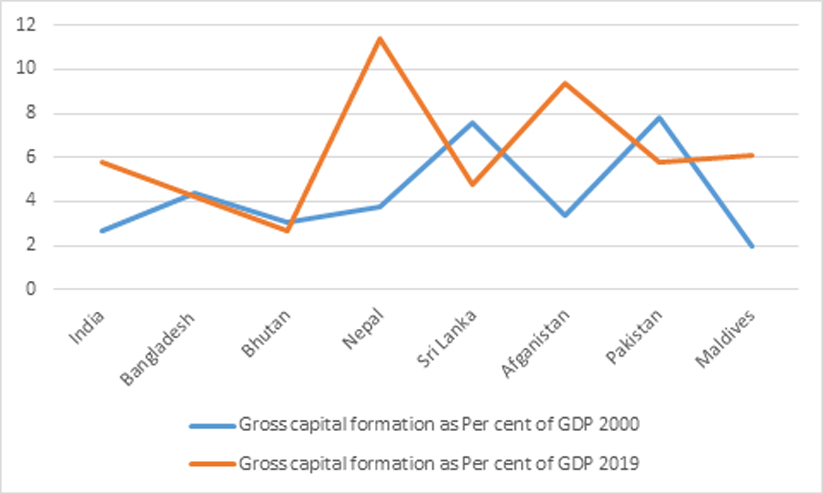

In an overall macro-economic sense, the growth of demand comes from household consumption and the rest comes from government consumption, gross capital formation, exports, and imports. Gross capital formation is reflective of investment demand in the economy and is the driver of consumption demand in the economy.

Data on the structure of demand between 2000 and 2019 shows that the share of gross capital formation in Gross Domestic Product at market prices has increased for all countries of the region except Bhutan, and Pakistan, while the growth of demand shows that both, the rate of growth of capital formation and household consumption has decelerated for most countries in the region.

Figure 1: Gross Capital Formation as per cent of GDP

Source: Asian Development Bank, Key Indicators Database,2020, https://kidb.adb.org

The growth and structure of sectoral aggregate-economic output, consisting of agriculture, industry, and services which drives the growth of incomes and demand shows that the share of agriculture in GDP has declined for all countries, while the services sector has grown except for in the Maldives.

The transformation through the growth of industries has not happened uniformly in the region. Pakistan, Bangladesh, the Maldives, and Bhutan are the countries where the share of industry in GDP has increased, while it has decreased in the other countries of the region.

Our assessment is based on the data (not separately presented here) shows that countries have experienced robust growth in GDP when there has been a balanced growth in all the sectors of the economy, which include agriculture, industry, and services - prompting that the growth strategy in the region will have to be a balanced one with an emphasis on all the three sectors. The experience of Bangladesh, Nepal, and the Maldives say so. The trends show that while total revenues have declined, tax revenues have increased for most countries except for Sri Lanka. Government expenditure as a proportion of GDP has increased for most countries except in Nepal, Afghanistan, and Pakistan.

On the aggregate fiscal side, most countries have witnessed an improvement in the overall budgetary balance except in Nepal, Afghanistan, and Pakistan. The message that goes out is that most countries have maintained a cautious stance on the budgetary front to the extent, it has been possible to do so. Most countries except Sri Lanka have shown an adverse position in terms of deficits on the trade (Export and import) and current account (which includes remittances and tourism and other current receipts) primarily due to excess imports over exports while the overall balance of payments (which includes the current account and capital account consisting of capital receipts by way of loan, commercial borrowings, and receipts from foreign investment) have shown an improvement for most countries except Afghanistan and Bhutan.

The adverse situation on the trade front due to excess imports over exports in most countries have been bridged by receipt of capital from abroad from remittances, other earnings and receipts on foreign loans and investment.The external debt service ratio as a proportion of earnings from exports of goods and services have also improved in the region except for Nepal, Sri Lanka, Maldives and Afghanistan

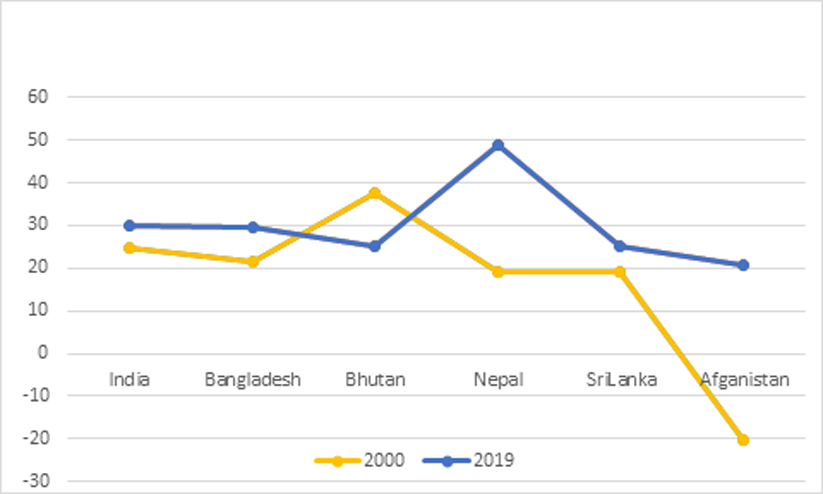

Figure 2: Gross National Savings as percent of GDP

Source: Asian Development Bank, Key Indicators Database,2020, https://kidb.adb.org

The Gross National Savings has improved for all countries of the region except Bhutan, while Gross Capital Formation for most countries have improved except Bhutan, Afghanistan and Pakistan. It must be recognized that although Gross Domestic Savings may have declined as a proportion of GDP in many countries, savings from their citizens abroad have bolstered the overall national savings of countries in the region. The data for the Maldives is not available.

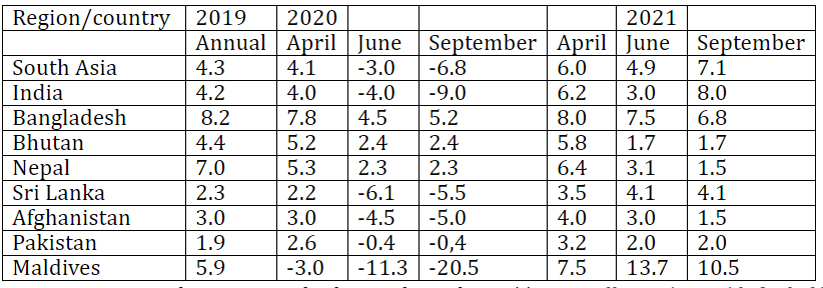

Table 2:Outlook for Growth rates(in percent) of GDP in South Asia

Source: Asia Development Outlook, Database,,htps://www.adb.org/sites/default files/publication/635666/adv2020-update .pdf

Positive outlook for Bangladesh, Bhutan and Nepal

South Asia’s 2020 GDP forecast is revised from 4.1 percent growth foreseen in April to-(-) 6.8 percent contraction in September 2020, as the pandemic spreads widely and containment measures are maintained. What gives the three economies of South Asia - Bangladesh, Bhutan, and Nepal a positive outlook? For that, we turn to the growth of demand in these countries for an answer between 2000 and 2019 to get an idea about the state of domestic demand in these countries before the pandemic.

Bangladesh witnessed positive growth in demand for all five categories as a proportion of GDP (household consumption, government consumption, gross capital formation, exports of goods and services and imports of goods and services)). Similar is the case with Nepal, while for Bhutan except for gross capital formation, all the four components of demand witnessed positive growth. The other countries have registered negative growth in more than one component of demand or have registered a steep fall in a single component.

So where has the South Asian economic strategy left the region with all its complexities? Each of the countries faces the problem of growing unemployment with low labour force participation rates.

Twin problems: COVID & economic revival

The economies face the two-fold problem of both combating the COVID-19 pandemic and economic revival. Both sets of problems have different approaches to resolution contradicting each other.

The COVID-19 pandemic calls for a lockdown/containment approach with the observation of proper health protocols which include hygiene, social distancing, and masking and the economic revival calls for unlocking and movement of goods and people.

In attempting the twin problem, countries often face a difficult choice as they may see a rise in the number of positive COVID-19 cases while they attempt to come out of the lockdown and take steps to the economic revival. Steps to control the pandemic will have to be firmly taken by ensuring adequate precautions, strengthening of health infrastructure to cope up with the growing cases of infection and the discovery of a vaccine.

The dilemma of growing COVID-19 cases and reviving economic activity is crucial at this juncture which the leadership in the South Asia region will have to resolve and, herein, lies the challenge for it.

Analysis has revealed that there is room for a more expansionary fiscal policy to boost consumption demand during these difficult times. What is needed is more aggressive policies to be created and protect jobs, by not only identifying new areas of investment in the rural areas to support supra-local linkages, but to also ensure generation of incomes, jobs, and local demand. This will help translate into the generation of higher demands in the sub-regional and regional levels and ultimately at the national level.

(The writer is a retired Indian Economic Service officer who worked in the labour ministry. He can be contacted at ppmitra56@gmail.com)

Post a Comment